Last week, a client came to us with a question that sounds simple, but catches many expats off guard. He had built a profitable consulting business in Dubai, kept his operations clean, and assumed the UAE’s tax-friendly system meant the story ended there. Then his home country issued a tax notice on the same income. His reaction was the same one we hear again and again: “How can this be taxed twice?”

That is where many people misunderstand the Double Taxation Agreement. The UAE does not impose tax on most personal income, which is one of the biggest reasons expats and foreign investors choose it. But many countries still tax their residents on worldwide income. Now that the UAE also applies corporate tax in certain situations, the risk of double taxation has become more real for business owners, investors, and self-employed professionals.

This is exactly why the UAE has signed Double Taxation Agreements with more than 100 countries. These agreements are designed to decide which country gets the primary right to tax certain income. They can also reduce tax rates, grant exemptions, or allow foreign tax credits so the same income is not taxed twice.

What Double Taxation Means

Double taxation happens when the same income is taxed by two different tax authorities. In simple terms, you pay tax twice on the same money.

This can happen in two main ways.

1. Corporate Double Taxation

This happens when a company’s profits are taxed first at the business level and then taxed again when those profits are paid out to owners or shareholders as dividends. A dividend is the part of a company’s profit that is distributed to its shareholders.

2. International Double Taxation

This happens when income is taxed in two different countries. One country may tax the income because it was earned there, while another country may tax the same income because the person or company is treated as a tax resident there.

The source country is the country where the income is earned.

The residence country is the country where the person lives for tax purposes or where the business is legally treated as resident.

Why Double Taxation Happens

Double taxation usually arises when tax rules in two countries overlap.

For example:

- One country taxes income based on where it is earned

- Another country taxes income based on where the taxpayer lives or is resident

- A person or company is treated as a tax resident in both countries

- There is no tax treaty in place to decide which country has the first right to tax the income

This matters because double taxation can reduce profits, increase tax costs, discourage foreign investment, and create unnecessary compliance problems for businesses and individuals.

That is exactly why the Double Taxation Agreement is so important. It helps define which country has the main right to tax certain income and what relief may be available when both countries have a claim.

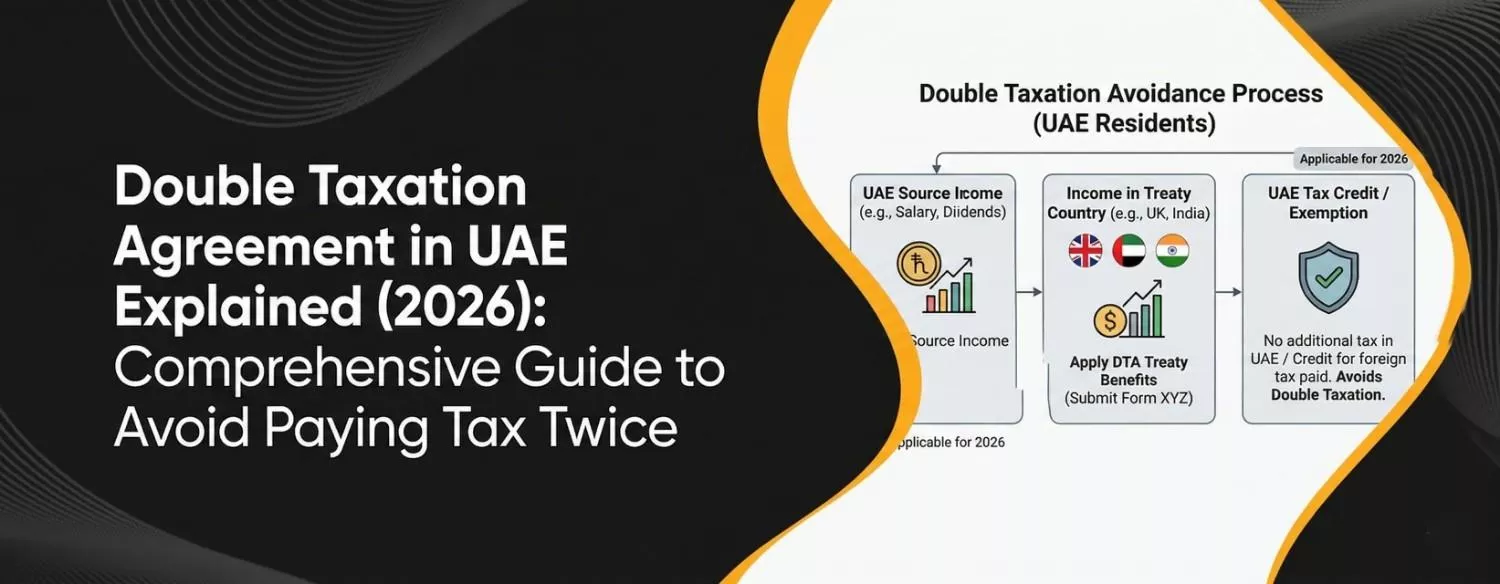

The Process: How to Claim DTAA Benefits

To benefit from these treaties, you must prove to the foreign tax authority that you are a tax resident of the UAE. This is done through a Tax Residency Certificate (TRC).

Step 1: Meet the Residency Criteria

- For Individuals: You generally need to have been physically present in the UAE for at least 183 days in a 12-month period. (Alternatively, 90 days if you have a permanent residence and a job/business in the UAE).

- For Companies: The legal entity must have been established in the UAE for at least one year.

Step 2: Apply via the Federal Tax Authority (FTA)

The process is handled digitally through the EmaraTax portal:

- Register: Create an account on the FTA EmaraTax portal.

- Submit Application: Select the service for “Tax Residency Certificate” and choose the specific country for which you need the DTAA benefit.

- Upload Documents: * Individuals: Passport, Visa, Emirates ID, Ejari (tenancy contract), and a “Report of Entry/Exit” from the immigration department.

- Companies: Trade license, Memorandum of Association (MOA), and audited financial statements.

- Pay Fees: The cost is typically AED 1,050 for individuals (unless you have a Corporate Tax TRN, which may reduce the fee).

Step 3: Present the Certificate

Once the FTA approves your application (usually within 5 business days), you download the digital TRC. You then provide this certificate to the tax authority or the paying entity in the foreign country to stop or reduce their tax deductions.

How to Avoid Paying Tax Twice

- Determine your tax residency: Identify whether you are a resident under UAE law and under your home country’s laws. Use the 183‑day rule or the centre‑of‑interests test. If dual residency arises, refer to the tie‑breaker rules in the relevant DTA.

- Check if a DTA exists: Verify that your home country has a DTA with the UAE. The Ministry of Finance and Titan’s treaty list provide updated lists.

- Obtain a Tax Residency Certificate: Apply online with the FTA and gather the required documents. This certificate is your evidence of UAE residence for treaty purposes.

- Understand the treaty provisions: Review the applicable DTA to know which income categories are exempt, what WHT rates apply and how to claim tax credits or exemptions. For example, Indian residents receive a full exemption on salary and capital gains, while South African residents must ensure their foreign income is taxed to qualify.

- Maintain documentation: Keep proof of taxes paid abroad, income sources, residency, TRC and any forms required by your home country. Failure to provide documentation is a common mistake leading to double taxation.

- Seek professional advice: Tax treaties can be complex. Consult an international tax adviser or chartered accountant to interpret treaty clauses, plan repatriation of profits, structure your business and avoid penalties.

The UAE’s Expanding Double Tax Treaty Network

The UAE has built one of the most extensive treaty networks in the region. As part of its wider economic strategy, the Ministry of Finance continues to expand both its Double Taxation Agreements, also called DTAs, and its Bilateral Investment Treaties, known as BITs, with major trade and investment partners.

A Double Taxation Agreement (DTA) is a treaty between two countries that helps prevent the same income from being taxed twice. A Bilateral Investment Treaty (BIT) is a separate agreement that protects investors and their investments when they operate across borders.

To date, the UAE has concluded 193 DTAs and BITs with key partner countries. These agreements are designed to make cross-border trade, investment, and business activity more secure and more tax-efficient.

In practical terms, these agreements can help by:

- reducing or removing taxes on certain types of income and profits

- protecting foreign investments from non-commercial risks

- allowing profits to be transferred freely in a convertible currency

Here, non-commercial risks mean risks created by government action rather than normal business loss. This can include nationalisation, where a government takes control of a private business or industry, and expropriation, where private assets are taken for public use, usually with compensation rules attached.

General Treaty Structure

Although each DTA is negotiated individually, most agreements follow the OECD model and include common elements:

- Allocation rules: which country taxes what income (employment, business profits, immovable property, pensions, etc.).

- Tax relief methods: e.g., exemption (income taxed only in one jurisdiction) or tax credit (tax paid in the source country credited against tax payable in the residence country).

- Withholding tax limitations: maximum rates for dividends, interest and royalties.

- Permanent establishment (PE) definitions: when a foreign company’s presence is significant enough to be taxed.

- Tie‑breaker rules: criteria to resolve dual residency issues based on centre of vital interests, nationality or place of effective management.

- Special provisions: shipping/air transport income, government service remuneration, pensions, and exchange‑of‑information rules.

How the UAE’s Tax Landscape Has Evolved

: Comprehensive Guide to Avoid Paying Tax Twice 1")

Unlike many jurisdictions, the UAE does not impose personal income tax. Salaries, rental income, capital gains, and inheritance earned by individuals or expats are exempt under domestic law.

The absence of personal tax is a major draw for foreign talent and investment. However, several changes mean double taxation is still a risk:

- Corporate tax introduction: With effect from 1 June 2023, the UAE takes a 9 % corporate tax on taxable profits above AED 375 000. This applies to UAE resident companies and to foreign entities operating via a permanent establishment (PE) in the UAE. Business profits can therefore be taxed both in the UAE and abroad unless a DTA provides relief.

- Withholding taxes abroad: Many countries impose withholding tax (WHT) on cross‑border payments such as dividends, royalties and interest. For example, the UK charges WHT on dividends paid to UAE residents unless a treaty reduces the rate. The UAE itself applies a 0 % WHT, but foreign WHT can still lead to double taxation unless the treaty allows credit or exemption.

- Changing international agreements: Tax treaties are periodically updated. Recent developments include a new Czech Republic‑UAE treaty in May 2023 (effective 2024), an amendment to the Austria‑UAE treaty effective January 2023, the expiry of the German treaty in June 2021 (There is currently no double taxation agreement between Germany and the UAE), and a new Russia‑UAE treaty announced by the Russian Ministry of Finance that applied from 1 January 2026. These shifts highlight the need to stay current.

Because of these factors, understanding and leveraging DTAs is crucial for businesses and individuals doing cross‑border work with the UAE.

How Double Taxation Agreements Give You Relief

A DTA helps make sure the same income is not taxed twice in two different countries. It does this in a few common ways.

1. Exemption Method

Under this method, one country agrees not to tax income that has already been taxed in the other country.

In simple terms, if one country has already taxed that income, the other country steps back.

For example, if a UAE tax resident earns income in another country, the treaty may say that only one of those countries can tax that income.

2. Tax Credit Method

Under this method, the country where you are a tax resident still taxes your income, but it gives you credit for the tax you already paid abroad.

This means you do not pay tax twice on the full amount.

For example, if a UAE company receives foreign income and tax was already deducted in another country, that foreign tax may be credited against the tax due, subject to the rules that apply.

3. Reduced Withholding Tax Rates

Many countries charge withholding tax on payments sent abroad, such as:

- dividends

- interest

- royalties

A withholding tax is a tax taken off the payment before the money reaches you.

A DTA may reduce that rate or remove it completely. This helps lower the overall tax burden on cross-border income.

4. Information Sharing and Anti-Abuse Rules

Modern tax treaties do more than reduce tax. They also include rules that allow tax authorities in different countries to exchange tax information and check whether a transaction is genuine.

This is meant to stop people from misusing treaties just to avoid tax.

One common rule is the Principal Purpose Test. This means treaty benefits can be denied if the main purpose of a deal or structure was only to get a tax advantage.

Who Can Benefit From a UAE DTA?

UAE DTAs can help many types of taxpayers involved in cross-border activity. This includes:

- public and private companies

- investment firms

- air transport companies

- UAE residents doing business internationally

- UAE-based businesses earning income from abroad

Individuals can also benefit. For example, a DTA may help if you:

- own property in another country

- receive a foreign pension

- work outside the UAE for a temporary period

- earn income from another country while living in the UAE

UAE Double Tax Treaties by Country: Highlights & Updates

| Country / Treaty | Status / Effective Date | Key Highlights |

|---|---|---|

| UAE Treaty Network Overall | As of mid-2025, the UAE had over 140 DTAs | The UAE’s treaty network covers many major trading partners across Europe, Asia, Africa, the Americas, and Oceania. |

| India–UAE DTAA | In force since 22 September 1993 | Applies to residents of India or the UAE. Covers Indian income tax and future UAE income or corporate taxes. Treaty benefits generally require 183 days in the UAE and a Tax Residency Certificate (TRC). India usually applies the tax credit method. Salary income of qualifying UAE residents is generally taxed only in the UAE under Article 15. Treaty rates include 10% on dividends, 5% on bank loan interest, 12.5% on other interest, and 10% on royalties. Capital gains from sale of Indian company shares by a UAE resident are taxable only in the UAE, while gains from Indian real estate remain taxable in India. |

| South Africa–UAE DTA | Updated in December 2016 | Allocates taxing rights for employment income, pensions, and investment income. It can provide relief for expats spending more than 183 days outside South Africa. |

| Russia–UAE Treaty | Entered into force in March 2026 and applies from 1 January 2026 | The new treaty is expected to give residents of both countries reduced tax rates and clearer taxing rights. |

| Czech Republic–UAE DTA | Signed on 24 May 2023, entered into force in May 2024 | Interest is taxed only in the country of residence. Royalties paid to a UAE resident are taxed at 10%. Dividends paid by the Czech Republic to a UAE resident are subject to 5% withholding tax, with exemptions for government entities. Capital gains from immovable property remain taxable where the property is located. |

| Austria–UAE Treaty Amendment | Effective from January 2023 | Amended to align with OECD standards. Changes include 10% withholding tax on dividends, mandatory exchange of banking information, and a Principal Purpose Test (PPT) to prevent treaty abuse. |

| Germany–UAE Treaty | Expired on 14 June 2021 and was not renewed | The 2011 treaty is no longer in force. German expats who became UAE residents before 1 January 2022 may still retain some treaty benefits, depending on their position. |

| United States | No DTA with the UAE | There is no double tax treaty between the UAE and the US. American citizens remain subject to US tax on worldwide income. There is, however, a separate Model 1 FATCA agreement for information reporting. |

| Other Non-Treaty Countries | No treaty position | Some countries still do not have a DTA with the UAE. |

Conclusion

With the UAE’s corporate tax era underway and a changing global tax landscape, understanding how DTAs work is more important than ever. By staying informed, obtaining the necessary residency documentation, and seeking expert guidance, you can turn complex tax rules into an advantage, ensuring that your income and profits are taxed only where they should be.

Consult a qualified tax adviser to understand how specific treaties impact your income, investments and business. With proper planning, you can legally reduce your tax burden, protect your wealth and invest confidently across borders.

Quick FAQs

Does the UAE tax personal income or capital gains?

No. The UAE does not impose personal income or capital gains tax. However, the introduction of corporate tax and possible changes in the future mean DTAs remain important.

Does the UAE have a double taxation agreement with South Africa?

Yes. The South Africa–UAE DTA, updated in 2016, allocates taxing rights and provides relief for residents. However, South African law now requires foreign income to be taxed abroad, so expats must prove non‑residency and obtain a TRC to enjoy the exemption.

Is there a double tax treaty between the UAE and the US?

No. There is no DTA between the UAE and the United States. US citizens and green‑card holders remain subject to US tax on worldwide income, though a FATCA intergovernmental agreement facilitates information sharing.

What if my country terminates its treaty with the UAE?

If a treaty lapses (as with Germany in 2021), taxpayers may revert to the domestic law of both jurisdictions. German residents moving to the UAE after 1 January 2022 cannot claim treaty benefits. Those who moved earlier may be grandfathered. Always check for updates.

How do I know which DTA provisions apply to my situation?

Review the treaty text or consult a professional. Consider factors such as your tax residency, type of income, presence of a permanent establishment, and whether you meet TRC requirements. Each treaty is unique and may vary in rates and exemptions.

Do DTAs apply to all seven emirates?

Yes. The treaties apply to the entire territory of the United Arab Emirates, including Abu Dhabi, Dubai, Sharjah, Ajman, Umm Al Quwain, Fujairah and Ras Al Khaimah.

Disclaimer: The information provided in this blog is for general informational purposes only. For professional assistance and advice, please contact experts.